The global IT market is entering another growth phase, with Gartner forecasting $6.15 trillion in IT spending in 2026 as AI investment continues to intensify. The forecast points to 10.8% year-over-year growth, building on momentum from 2025 and reflecting sustained demand across enterprise, cloud, and service-provider markets.

What stands out in this outlook is how spending is shifting beneath the surface.

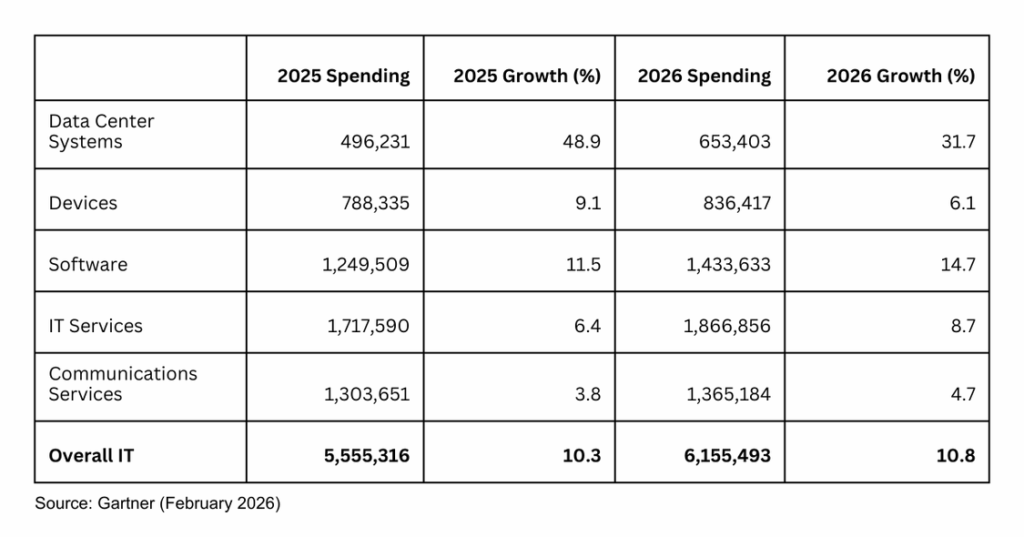

Investment is becoming increasingly concentrated in data centers, servers, and AI-related software, while more mature categories, particularly end-user devices, are starting to cool. The result is a market that’s less about broad-based expansion and more about building the foundational layers needed to support AI at scale.

Why It Matters: For enterprise IT leaders, this forecast is really about choices that will stick. AI spending is pulling more budget into data centers, servers, and core software platforms, which means today’s infrastructure and vendor decisions will shape costs and flexibility for years. As hyperscalers soak up AI capacity and generative AI moves out of pilots and into real operations, IT teams are under pressure to make the cloud, governance, and security pieces work together at scale. Slower device growth doesn’t change much, but it reinforces that 2026 is more about building durable foundations rather than chasing quick wins.

- AI infrastructure continues to be the primary growth engine: Server spending is forecast to increase 36.9% in 2026, driven largely by hyperscale cloud providers expanding capacity for AI training and inference. Despite ongoing concerns about an AI bubble, spending across AI-related hardware and software remains strong, suggesting demand is still outpacing supply.

- Data centers are absorbing a growing share of global IT budgets: Spending on data center systems is forecast to rise 31.7% year over year, pushing total spending beyond $650 billion in 2026, up from just under $500 billion the year before. This reflects the scale of compute, storage, and networking required to support AI workloads, as well as continued cloud expansion.

- Software spending remains resilient: Gartner forecasts total software spending will exceed $1.43 trillion in 2026, with growth of 14.7%, slightly lower than earlier expectations but still among the strongest rates across IT segments. Enterprises continue to invest in application software and infrastructure platforms that enable automation, analytics, and AI-driven capabilities.

- Generative AI spending stands out as a major growth driver within software: Spending on GenAI models is forecast to grow 80.8% in 2026, with their share of the overall software market increasing by 1.8%. This points to a shift away from experimentation toward more consistent, production-level use of GenAI across industries.

- Device spending continues to grow, but at a slower pace: Total spending on devices is forecast to reach $836 billion in 2026, with growth slowing to 6.1%. Rising memory prices are pushing up average selling prices, discouraging replacement cycles, and contributing to shortages at the lower end of the market, where margins are thinner.

- IT services and communications services deliver steady growth: While these segments don’t match the pace of infrastructure or software, they remain essential as organizations rely on consulting, integration, managed services, and connectivity to deploy and operate complex IT and AI environments.